Fitch Ratings: Coronavirus Could Put Natural Gas Market under Severe Stress

Wednesday, February 12 2020 - 07:20 PM WIB

(Fitch Ratings-London/Chicago/New York-11 February 2020)--The coronavirus outbreak could put the natural gas markets in Europe and Asia under severe stress due to the curbing of liquefied natural gas (LNG) imports by China, Fitch Ratings says. This could significantly delay the supply-demand rebalancing expected in 2020. The credit impact will depend on the duration of demand loss and any contract price renegotiations.

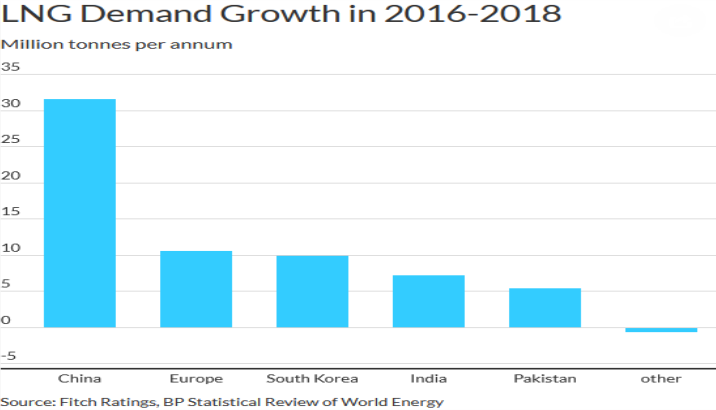

Some Chinese importers of LNG have declared 'force majeure' on their contracts, which may cancel up to 70% of seaborne imports in February, according to press reports. Chinese LNG imports were the key driver in the market: the country accounted for 17% of global purchases in 2018 and 50% of global demand growth in 2016-2018. The magnitude of any demand loss will depend on the speed of business activity recovery.

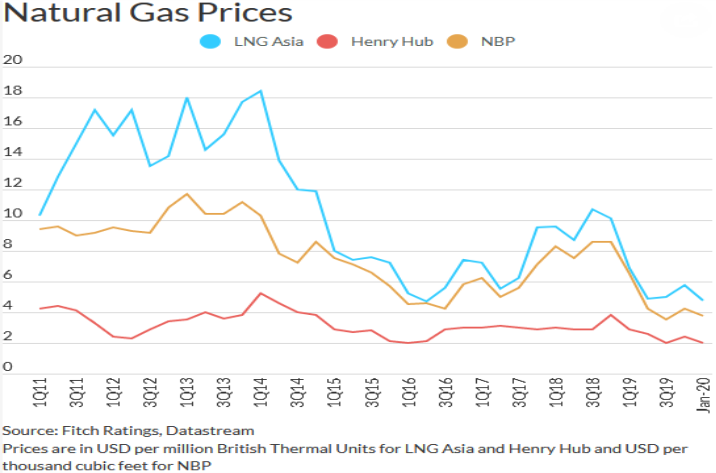

The National Balancing Point (NBP) and Asia LNG prices dropped to around USD3.0/mcf on the force majeure news (from January averages of USD3.8/mcf for NBP, already a record low for winter, and USD4.8/mcf for Asia).

The market was already oversupplied in 2019 due to LNG capacity additions in Australia and more recently Russia and the US, and slower growth in Chinese LNG imports. This was exacerbated by warm weather in Europe and Asia and the high level of gas storage in Europe. Average spot prices almost halved as a result in 2019 compared to 2018.

Despite the pressures, we do not anticipate prices in Europe and Asia falling and remaining below USD3.0/mcf as this level will not cover half-cycle production costs for US and other producers. Such a level would result in production shut-ins and reduced supplies. A prolonged period of low spot prices could spark contract re-negotiations between suppliers and customers in Asia, where contracts are oil-linked, and slow down prospective projects.

Rating implications for large Chinese energy companies are unlikely due to the latter's linkage with the state and conservative credit metrics. Gas and electricity account for only 5% of the EBITDA of CNOOC, which is the largest LNG importer in China. We do not expect Chinese national oil companies to significantly lower domestic gas production (which accounted for 58% of domestic gas demand in 2019), but assume they will first try to lower LNG imports, which are more costly.

Weak gas prices in Europe and the inflow of LNG imports could have a negative impact on Gazprom's operating cash flows in 2020. Around two-thirds of Gazprom's contracts are fully or partially linked to spot or forward gas prices, and the present price levels could make some exports unprofitable. This may exert pressure on Gazprom's standalone profile, but its final rating is linked to Russia and unlikely to be affected. Novatek's Yamal LNG project supplies both the European and Asian markets, but its contracts are predominantly oil price-linked.

The performances of oil majors, including Shell, Total and BP, are mostly driven by oil rather than gas prices. We estimate that in 2018 liquids accounted for 75% of Shell's upstream revenue, and according to the company more than 80% of its long-term LNG portfolio is linked to oil prices. The present gas market pressures alone would not lead to negative rating actions for oil majors, as long as Brent does not fall significantly below USD50-55/barrel for a prolonged period.

Independent producers with high gas exposure could be more affected, though much depends on individual circumstances. Neptune Energy's upstream portfolio is skewed towards natural gas, but its revenue is almost equally driven by spot oil and gas prices. It also has some leverage headroom within its rating.

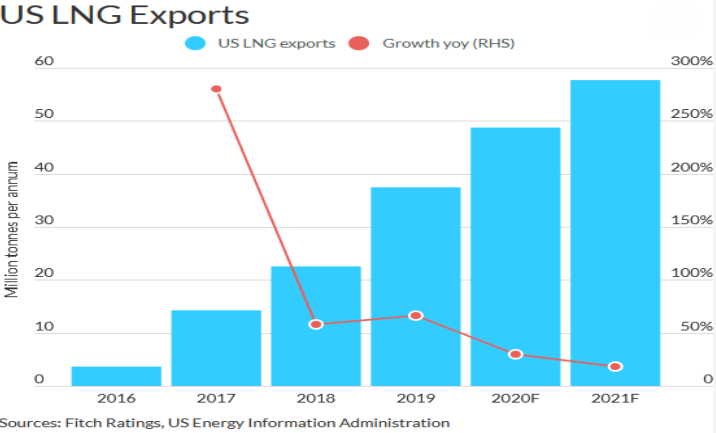

Few US LNG projects will be directly affected by the force majeure given the lack of deliveries to China amid trade tensions. US supplies are expected to grow in 2020-2021 thanks to capacity additions, although with lower growth rates. However, prices falling below USD3/mcf could force some production shut-ins (assuming a Henry Hub price of around USD2/mcf and shipping costs of around USD1/mcf), and delay final investment decisions on the next wave of projects scheduled to come on-stream from 2023. (ends)