Indonesian Hydrogen Outlook 2024

Thursday, December 28 2023 - 06:55 AM WIB

by: William Jhanesta

Key Findings:

- The announced production capacity of low-carbon hydrogen projects reached 3.18 million tons per annum (MTPA) by the end of 2023, with an estimated total investment value of approximately US$ 35.75 billion.

- Geothermal energy has emerged as the predominant renewable energy source for green hydrogen feedstock, accounting for 25% of the total announced production capacity.

- The top three locations dominating the announced production capacity are North Sumatra, East Kalimantan, and South Sumatra, which account for 35%, 18%, and 11% of the planned production capacity, respectively.

- Several global electrolyzer providers, including ThyssenKrupp, Nel, John Cockerill, and Siemens Energy, have shown interest in market opportunities in the country, although none have yet secured a deal.

- The ammonia industry is expected to play a significant role as a consumer of hydrogen, with its demand projected to reach 2 MTPA by 2060.

- There are ongoing opportunities in the hydrogen export market, with substantial demand anticipated from Singapore, South Korea, Japan, and other regions, positioning Indonesia as a key player in the global hydrogen landscape.

The year 2024 marks a critical juncture in shaping the future trajectory of the hydrogen industry in Indonesia. Significant developments are expected during this year, including the establishment of a regulatory framework, the creation of a national hydrogen roadmap, and market reactions, all directed towards establishing a concrete hydrogen ecosystem in the country. In this brief overview, we examine the current state of hydrogen development in Indonesia as of the end of 2023 and outline the anticipated developments for the forthcoming year.

Announced Capacity Continues to Increase.

The announced capacity for the low-carbon hydrogen market in Indonesia has continued to increase in recent years, indicating a robust movement towards green hydrogen projects. These projects are produced through the electrolysis of water using renewable energy. According to Petromindo's Hydrogen Database, by the end of 2023, over 50 low-carbon hydrogen projects had been announced. Of these, 36 disclosed their planned production capacity, totaling approximately 3.18 million tons per annum (MTPA). This total consists of 2.03 MTPA of green hydrogen and 1.15 MTPA of blue hydrogen.

North Sumatra, East Kalimantan, and South Sumatra are leading the way in Indonesia's low-carbon hydrogen projects, contributing 35%, 18%, and 11% to the planned production capacity, respectively. These regions are highly favored due to their plentiful renewable energy resources, which are essential for green hydrogen development, and their depleted reservoirs, which are well-suited for storing CO2 from hydrogen production activities based on natural gas. The versatility of hydrogen is expected to drive further market growth in other regions as well.

Source: Petromindo Data Analysis

In the context of electricity sources for green hydrogen, geothermal energy is currently leading in development plans, accounting for 25% of the total announced production capacity. According to Petromindo's internal conversion factor, the estimated energy requirement from geothermal sources to support the planned projects is approximately 31,697 gigawatt-hours (GWh).

Solar and wind-based hydrogen production are expected to see significant growth in the coming years, benefiting from their cost-effective characteristics. A recent study by IRENA highlights substantial cost reductions in solar and onshore wind power, estimated at around 22% and 38%, respectively, compared to their average prices in 2009. Regarding investment value, not all projects have provided detailed breakdowns of their capital expenditure requirements. Based on assumptions derived from publicly available data, Petromindo estimates that the total investment needed to realize the 3.18 MTPA hydrogen production capacity is around US$ 35.75 billion. This figure comprises approximately US$ 27.24 billion for green hydrogen projects and the remaining US$ 8.33 billion for blue hydrogen projects.

Notable Hydrogen Announcements in 2023.

In 2023, Petromindo has identified significant announcements in Indonesia's hydrogen production plans and realizations, involving major players such as Pupuk Indonesia, PLN, Pertamina, ACWA Power, and Augustus Global Investment.

PT Pupuk Indonesia (Persero), a state-owned fertilizer company, recently reaffirmed its commitment to a higher green and blue hydrogen initiative, aiming to produce and/or consume a total of 2.3 MTPA of green and blue hydrogen. This initiative is aligned with the company's low-carbon ammonia program.

While in relatively modest quantities, PT PLN (Persero) stands out as the first in the region to operationalize hydrogen production plants. Currently, PLN operates 21 green hydrogen production facilities with a combined production capacity of 199 TPA and 124 TPA of excess hydrogen. All hydrogen plants are powered by renewable energy, including supplies from rooftop solar plants and Renewable Energy Certificates (RECs) generated from the Kamojang geothermal power plant (140 MW) and Bakaru hydropower plant (130 MW). Leveraging its ownership of the national electricity system network, PLN can produce hydrogen at a low cost without additional investment in new power plants.

During COP28 in Dubai, Pupuk Indonesia, PLN, and UAE-based ACWA Power unveiled plans for a US$ 1 billion green hydrogen production facility called Garuda Hidrogen Hijau (GH2) in Gresik, East Java Province. The site is set to be powered by 600 MW of solar and wind power plants, with operations expected to commence in 2026.

Source: Petromindo Data Analysis

Augustus Global Investment, a company based in Germany, revealed its plans in August 2023 to develop a green hydrogen project in the Arun Special Economic Zone, located in Aceh Province. The project is expected to have a renewable energy capacity of 300 MW and has received technical and economic feasibility endorsement from global consultants Black & Veatch. With a total investment of USD 500 million, this project represents a substantial addition to Indonesia's expanding hydrogen industry.

PT Kilang Pertamina Internasional, the refinery and petrochemical subsidiary of PT Pertamina (Persero), recently unveiled plans to construct a blue ammonia facility in Bintuni Bay, West Papua Province. This plant is anticipated to commence operations in 2030, aiming for a production capacity of 875,000 TPA (tons per annum) of blue ammonia, which is equivalent to approximately 150,000 TPA of blue hydrogen. The facility is designed to process 90 million standard cubic feet per day (MMSCFD) of natural gas and will be integrated with a carbon capture system.

However, there is still a considerable amount of work to be done in the future.

Despite the remarkable increase in total announced project capacity, showing a significant growth of approximately 489% over the past two years, the current state of hydrogen project development in Indonesia largely remains in the early stages. This situation is quite expected, given that the clean hydrogen market in Indonesia only started to emerge in 2021, lagging behind global development initiatives that had begun earlier.

According to Petromindo, over 85% of the total announced projects are still in the planning phase. These projects are distributed across various stages of development: 63% in the pre-feasibility study phase, 22% in the feasibility study phase, and 13% in the pre-final investment decision (Pre-FID) phase. It is noteworthy that the projects in more advanced stages of development tend to be relatively small and are mostly spearheaded by a few of the more established industry players.

Source: Petromindo Data Analysis

Petromindo estimates that approximately 0.06 MTPA (million tons per annum) of capacity from advanced-stage projects will reach the Final Investment Decision (FID) within the next 12 months. This figure could increase to around 0.09 MTPA by the end of 2024, dependent on swift advancements in grid-connected clean hydrogen and hybrid hydrogen projects, especially those at the Ulubelu and Kujang Cikampek plants.

To maximize the potential of clean hydrogen, particularly green hydrogen, the Indonesian government should consider using on-grid renewable electricity, especially from systems with oversupply. This approach could significantly reduce the production costs of green hydrogen. Currently, electricity contracted with PLN through power purchase agreements (PPAs) cannot be used for hydrogen production, even when the power generation systems have the capacity to exceed the supply specified in the contracts.

The Ministry of Energy and Mineral Resources indicates that the production cost of low-carbon hydrogen in Indonesia is still relatively high, ranging between US$ 5-10 per kg. While specific onsite production costs may drop to as low as US$ 2.3 per kg under certain conditions, this is still above the global benchmark of US$ 2 per kg needed for widespread market acceptance. Therefore, government intervention through a robust regulatory framework is crucial to achieve more competitive low-carbon hydrogen production costs.

Considering the significance of geothermal energy as the main feedstock for green hydrogen projects in Indonesia, the government should explore the option of auctioning geothermal concessions specifically for green molecule development. This approach aligns with the broader goal of diversifying the geothermal business landscape.

Major international companies, including Chevron and Mubadala, have shown a strong interest in Indonesia's geothermal resources, particularly for their potential in the green hydrogen sector. The issuance of permits tailored to green hydrogen development could address current challenges in geothermal development. This would not only accelerate geothermal project timelines but also enable developers to market green hydrogen at a premium, enhancing the sector's overall sustainability and expansion.

Identified hydrogen technology provider for Indonesian market

Hydrogen technology is adapting to market demands, with two primary types currently dominating the market: small-scale production systems and large-scale industrial technologies, each suited to specific resource availabilities and market needs.

Small-scale production systems are designed for quick deployment, relatively straightforward installation, and cost-effective solutions. Conversely, large-scale industrial technologies emphasize system optimization, reliability, and cost efficiency, particularly for larger production volumes.

The diversity of renewable feedstocks announced for green hydrogen production suggests a need for a variety of electrolyzer technologies. These technologies must be compatible with the capacity factor and efficiency of each type of renewable energy source.

Among the 36 projects listed in our hydrogen database, totaling a production capacity of 3.18 million tons per annum (MTPA), Petromindo estimates that a total investment of USD 35.75 billion is required for upstream hydrogen investments. Of this investment, a substantial portion, USD 6.85 billion, is expected to be allocated to electrolyzers, which are the devices used to split water molecules into hydrogen and oxygen.

At the recent Petromindo Hydrogen Conference 2023, several electrolyzer manufacturers expressed their interest in joining the burgeoning hydrogen market in Indonesia. These manufacturers include ThyssenKrupp, Topsoe, SFC Energy, Enapter, Siemens Energy, and Advent Technologies.

Source: 360 Quadrant, Petromindo Data Analysis

However, as of now, potential participants for blue hydrogen production in the Indonesian market have yet to be identified. Leading global steam-methane reforming (SMR) providers, including Linde, Air Liquide, and Air Products, are likely candidates to capitalize on the emerging blue hydrogen sector. They can leverage their extensive experience and strong portfolios in grey hydrogen within Indonesia to make a significant impact in this growing market.

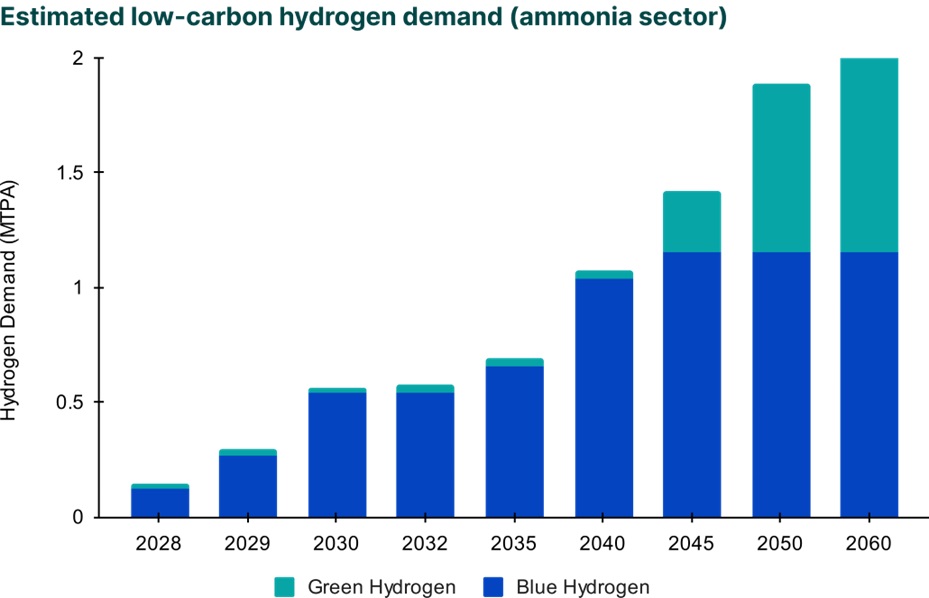

Demand will largely depend on ammonia producers.

In Indonesia, the current production capacity of grey ammonia is estimated at 8 million tons per annum (MTPA), with the Pupuk Indonesia Holding Company being the largest producer. Other significant participants in this sector include private entities like Kaltim Parna Indonesia and ESSA Industries Indonesia.

Petromindo forecasts that for at least the next decade, the ammonia industry will be a leading sector within the clean hydrogen producer market. This projection is based on the fact that the low-carbon ammonia production system mainly requires substituting carbon-intensive hydrogen with cleaner hydrogen options, rather than undergoing substantial technological changes. Our models suggest that by 2060, the estimated demand for low-carbon hydrogen will reach 2 MTPA. The demand for blue hydrogen is expected to level off starting in 2045, influenced by the increasingly competitive production costs of renewable energy, which facilitates the production of cleaner green hydrogen.

Given Pupuk Indonesia's strong presence in the industry, the company is anticipated to play a crucial role in utilizing the produced low-carbon hydrogen in Indonesia. Petromindo anticipates that over 85% of the hydrogen demand will be met by this state fertilizer company, with the rest being taken up by Pertamina and other private ammonia producers.

Source: Petromindo Data Analysis

The number of announced hydrogen export projects is expected to grow further.

Low-carbon hydrogen serves a dual purpose: it's a critical component in domestic decarbonization strategies and is increasingly becoming a viable product in the international market. This significance arises from the understanding that not every country has the natural resources necessary to meet their energy requirements.

Indonesia is emerging as a key player in the green hydrogen sector, strategically positioned as a potential hub. Its geographical location near high-demand areas such as Singapore, Japan, and South Korea highlights its potential as a significant exporter of low-carbon hydrogen. With numerous countries indicating their intention to become net hydrogen importers, Indonesia is well-placed to capitalize on this trend and actively participate in the global hydrogen market.

Petromindo has identified at least five projects within the announced low-carbon hydrogen projects that are designated for the international market. These include the development of solar-based hydrogen in Batam for export to Singapore and the Lahendong hydrogen project aimed at the Japanese market.

To realize this goal, the Indonesian government must make specific preparations, focusing particularly on providing regulatory certainty for the export of these green molecules. A practical approach would be to adopt regulatory frameworks similar to those in place for ammonia export activities. Furthermore, the government should support the development of infrastructure necessary for distributing hydrogen to neighboring countries in the Southeast Asian region. This includes establishing hydrogen pipelines. Alongside technical and financial assistance, the government, via the relevant ministries, needs to develop regulations and standards to ensure the safe distribution of hydrogen.

To obtain more comprehensive and detailed information regarding the hydrogen business outlook in Indonesia, get Indonesian Hydrogen Report 2024, here.